The world is entering a new phase of technological development, characterized as industry 4.0. This is a perfectly new reality, in which the role of human capital increases unprecedentedly. In this situation, the presence of an advanced university system becomes a consequence of a high level of social development and the foundation for the future progressive transformation of society. Under these conditions, the inequality of national university systems becomes especially dramatic because weak higher education establishments deprive their nations of the possibility to enter into the new technological era. This circumstance increases competition between universities of different countries, which, in turn, leads to changes in the intellectual disposition, developed in recent decades, not only between individual states but also between large geographical regions.

In 2017, work on the identification of world–class universities (WCUs) began, resulting in the compilation of two specialized international rankings [1, 2] and respective analytical materials [3, 4]; in 2019, this work continues. Our task in this case is to clarify the existing situation in the global market of leading universities (MLU), as well as to determine the geopolitical meridians of further “castlings” in national university systems.

The structure of the world university sector. Just like in our previous publications [3, 4], we will proceed from the assumption that MLU consists of three segments: U–1, U–2, and U–3. The U–1 group is formed by universities that meet two conditions: first, they are in the Top 100 by at least one of the existing global university rankings (GURs) and, second, they are in the Top 50 by at least five subject ratings according to QS data. The U–2 group comprises higher education establishments that claim a WCU status; i.e., they meet the first condition but not the second one. The U–3 group consists of specialized world–level institutes that do not meet the first condition and only partially meet the second one. Each leading higher education establishment receives a quantitative estimate of its achievements in the global market (H), the summation of which gives an integrated estimate of national university systems (W) [3]. This classification makes it possible to determine clearly the circle of global players of the world market of universities and to assign a quantitative quality measure to each of them.

Let us explain the meaning of the three-sector structure of the MLU. Its skeleton is formed by WCUs characterized by a high quality of studies and education over a wide circle of scientific disciplines. We can say that WCUs have a certain height (depth) and breadth of scientific activity. The direct competitors of WCUs are higher education establishments of group U–2, which have reached a high scientific level but within a more limited range of professional trends. Finally, the reserve to be added to WCUs is higher education establishments of group U–3, which have also been recognized internationally, but only in individual scientific disciplines. Competition in the MLU manifests itself in castlings between higher education establishments of the above three groups: some WCUs lose their status, giving way to institutes from group U–2, while higher education establishments of group U–3 widen the scope of their scientific interests and with time turn into full–fledged WCUs.

As before, the computations used data of the most authoritative global rankings–Quacquarelli Symonds (QS), Times Higher Education (THE), Academic Ranking of World Universities (ARWU), the Center for World University Rankings (CWUR), and National Taiwan University Ranking (NTU). The main indicators in the computations performed are the number of higher education establishments and the “force” index of concrete universities (H) and countries (W). The goal of this research is to understand the dynamics of changes taking place in 2017–2019.

This two–year interval is of special significance due to the ongoing large–scale reformatting of the world university system. This process is determined by the fact that the world economy has entered the epoch of global turbulence, when the old leader, the United States, is weakening but no new leader has appeared to replace it. The analysis of MLU is of special interest due to its specifics as well. The point is that, although the presence of WCUs ensures economic growth, their appearance itself is as a rule the final chord of the long-standing successful economic development of a country. The appearance of global universities always follows economic achievements but never precedes them. In this context, the long–standing rise of China, South Korea, and Germany was bound to affect the MLU, as well as the long–standing stagnation of Japan and the weakening of the economic hegemony of the United States. In a sense, WCU geography makes it possible to design a new geopolitical map of the world and global universities themselves, to make a rather precise diagnostics of the true economic and political power of various countries and regions.

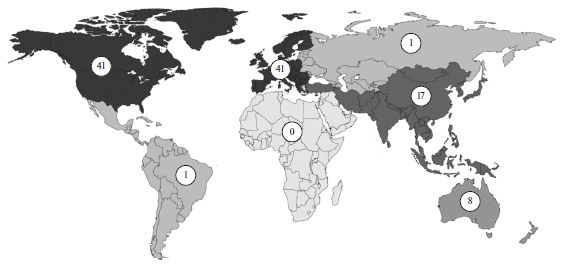

Reformatting the global university market. Let us analyze the MLU in view of major regions of the world (Table 1). For the sake of convenience, we use special associations of countries. For example, the Greater China group includes universities of China, Taiwan, Hong Kong, Macau, and Singapore, which to an extent represent Chinese civilization; the “Small British Union” (SBU) comprises universities of the United Kingdom and its former English-speaking colonies–the United States, Canada, Australia, and New Zealand, which form a relatively homogeneous cultural space. Table 1 shows the number of global universities of each of the three types, the last column representing the generalized index of national university systems in points (W). The obtained results make it possible to plot the map of WCUs and identify several key trends in the development of the MLU (Fig. 1 shows the number of WCUs in respective regions of the world, for example, the United States + Canada, Europe, Australia + New Zealand, etc.).

Table 1. Comparison of the university systems of major regions of the world

|

Country |

2017 |

2019 |

||||||

|

U–1 |

U–2 |

U–3 |

W |

U–1 |

U–2 |

U–3 |

W |

|

|

United States |

38 |

16 |

36 |

371.2 |

36 |

14 |

47 |

346.7 |

|

Small British Union |

67 |

19 |

106 |

562.7 |

67 |

15 |

115 |

549.3 |

|

Europe without Britain |

19 |

21 |

75 |

77.8 |

23 |

18 |

100 |

90.8 |

|

All of Europe |

36 |

22 |

114 |

204.3 |

41 |

18 |

141 |

229.2 |

|

“Greater China” |

11 |

1 |

19 |

44.3 |

11 |

3 |

19 |

49.1 |

|

Asia |

19 |

4 |

39 |

75.9 |

17 |

8 |

35 |

77.3 |

|

Latin America |

1 |

1 |

10 |

6.1 |

1 |

1 |

9 |

5.3 |

|

Middle East |

0 |

2 |

1 |

1.6 |

0 |

1 |

2 |

1.1 |

|

Africa |

0 |

0 |

4 |

0.6 |

0 |

0 |

3 |

0.4 |

|

Russia |

1 |

0 |

4 |

1.7 |

1 |

0 |

2 |

1.3 |

First, the university system of Asia has begun to fall behind that of Europe (without Britain). The point is that in 2017 the WCUs of continental Europe and Asia became equal in number, and it seemed that in the near future Asian countries would steadily increase their potential at the expense of the weakening Europe [4]. The past two years have confuted this supposition. The Asian miracle has proved to be unstable, and Asia has lost two WCUs, while Europe has increased its potential rather sharply: there appeared not only four new WCUs there but also 25 new specialized world– level institutes. Thus, Europe is gaining heft, creating not only multifunctional WCUs but also U–3 higher education establishments due to point successes in individual sciences. This makes it possible to conclude preliminarily that a university Reconquista has begun in Europe. Characteristically, the core of the Asian system that used to make it stable was Greater China, which has somewhat improved its positions.

Second, the university systems of the United States and the European Union (including Britain) were fully reformatted, which was manifested in a change in the dominant regional group. For example, in 2017, the number of US WCUs surpassed by two units the number of European ones, while in 2019 Europe prevailed by five units. Possibly, this was the beginning of the decline of the era of the American university system and the yielding of the palm to Europe. In parallel, the number of WCUs in North America and Europe became fully equal (Fig. 1). This circumstance confirms the previously made conclusion about a new upward wave of higher education in the Old World.

Fig. 1. Geography of world–class universities.

Third, the MLU is increasingly concentrating in three segments of the world–Europe, Asia, and SBU; the role of the rest of the Earth is vanishingly small and continues to diminish. One can easily see that the situation with global universities has clearly worsened in Latin America, Africa, the Middle East, and the post–Soviet space. Note that the entire African continent and the Middle East are fully outside the sphere of WCUs, while Latin America and the post-Soviet space have only one such university each, in Brazil and in Russia, respectively. In 2019, the share of the four regions–Latin America, Africa, the Middle East, and the post–Soviet space–in the WCU market was 1.6% of their total number and 0.9% by the aggregate potential of the university system W.

It is extremely important geopolitically to fix the rise of the European university system. In particular, G. Arrighi’s fifth cycle of accumulation is building up at present in China and neighboring territories [5, 6]. However, the continuation of the trend toward the relative strengthening of Europe may mean that the center of world capital is not shifting from the United States to Asia but is returning to the Old World. This fact cardinally changes the process of world capital recirculation.

The drivers of the university system of Asia. The more than 30–year growth of China has turned it, together with the rest of Asia, into a key player in the global market of higher education. In only two years, China has managed to bring to market still another WCU, which makes five, and, in addition, to “raise” two higher education establishments that claim this status (Table 2). This dynamic has allowed China to become the absolute leader in the Asian MLU, although it was in second place only two years ago, noticeably behind Japan. Most likely, this castling is final, and the leadership of China will be strengthening in the years to come, making it the main driver of the region’s upturn. If we add to China the dwarfish formations on its territory–Hong Kong and Macau– and the disputed Taiwan and Singapore, where the ethnic Chinese amount to more than 75% of the population, the potential of its university system will be record breaking. Yet even without Singapore, Greater China has nine WCUs; i.e., it is third in the world after the United States and Britain.

Table 2. Comparison of the university systems of Asian countries

|

Country |

2017 |

2019 |

||||||

|

U–1 |

U–2 |

U–3 |

W |

U–1 |

U–2 |

U–3 |

W |

|

|

Japan |

5 |

2 |

2 |

18.7 |

3 |

2 |

6 |

16.4 |

|

China |

4 |

1 |

13 |

14.5 |

5 |

2 |

12 |

18.9 |

|

Singapore |

2 |

0 |

0 |

13.4 |

2 |

0 |

1 |

14.5 |

|

Hong Kong |

4 |

0 |

3 |

12.9 |

3 |

1 |

3 |

12.9 |

|

Macau |

– |

– |

– |

– |

0 |

0 |

1 |

0.1 |

|

Taiwan |

1 |

0 |

3 |

3.5 |

1 |

0 |

2 |

2.5 |

|

South Korea |

3 |

1 |

6 |

10.8 |

3 |

2 |

6 |

10.5 |

|

Malaysia |

0 |

0 |

4 |

1.2 |

0 |

1 |

1 |

0.9 |

|

India |

0 |

0 |

4 |

0.4 |

0 |

0 |

3 |

0.3 |

|

Turkey |

0 |

0 |

2 |

0.2 |

– |

– |

– |

– |

|

Indonesia |

0 |

0 |

1 |

0.1 |

– |

– |

– |

– |

|

Thailand |

0 |

0 |

1 |

0.1 |

– |

– |

– |

– |

|

Total |

19 |

4 |

39 |

75.9 |

17 |

8 |

35 |

77.3 |

The next driver of Asia in terms of significance is Japan, but its position is rapidly worsening. As opposed to China, the Land of the Rising Sun has been close to depression over the past 30 years, which tells on its university system. The fact that the number of Japanese WCUs has decreased by two units over two years shows that it has lost its driving force. Moreover, the third driver of the Asian block, South Korea, is actively claiming Japan’s position and, most likely, will soon oust it to third place.

Amazing is Singapore with its two powerful WCUs, which is undoubtedly a miracle. Such an achievement is unprecedented for an island microstate, but this is not the whole story. Securing 20th position in the WCU ranking for the National University of Singapore, it has promoted Nanyang Technological University from 25th to 24th place over two years and has created another specialized WCU on its territory. Thus, despite its small size, Singapore acts not only as a full–fledged country driver of the Asian university system but also as a model for all its participants.

The presence of Greater China, Japan, and South Korea in Asia makes it a full–fledged player in the global MLU. However, one should recognize that the geography of its WCUs is rather narrow. Countries such as India and Malaysia are just making halfhearted steps to enter the global university market, and the first achievements of Indonesia, Thailand, and Turkey on this road have proved to be extremely unstable.

Competition and collaboration in the European university system. Over the last two years, Europe has again demonstrated its viability and creativity. Its achievements are due to the wide geographical diversification. For example, the MLU of Asia in 2019 was represented by only nine geographical jurisdictions; if we consider Hong Kong, Macau, and Taiwan to be part of China, this number is reduced to six. In Europe, 16 states make a worthy contribution to the regional potential (Table 3), which allows it to advance massively in all directions, from the creation of specialized higher education establishments to the concentration of research in large WCUs.

Table 3. Comparison of the university systems of European countries

|

Country |

2017 |

2019 |

||||||

|

U–1 |

U–2 |

U–3 |

W |

U–1 |

U–2 |

U–3 |

W |

|

|

Switzerland |

2 |

3 |

9 |

16.9 |

3 |

2 |

16 |

17.9 |

|

Netherlands |

5 |

4 |

5 |

14.6 |

4 |

6 |

5 |

15.5 |

|

Germany |

6 |

2 |

8 |

13.5 |

6 |

4 |

14 |

17.7 |

|

Sweden |

2 |

3 |

6 |

7.1 |

3 |

1 |

8 |

6.9 |

|

Denmark |

2 |

0 |

5 |

6.0 |

2 |

0 |

4 |

6.4 |

|

France |

0 |

2 |

10 |

5.0 |

2 |

1 |

14 |

8.2 |

|

Belgium |

1 |

1 |

2 |

3.8 |

1 |

1 |

2 |

4.6 |

|

Italy |

0 |

3 |

5 |

3.4 |

0 |

2 |

10 |

4.7 |

|

Spain |

0 |

1 |

8 |

2.2 |

0 |

1 |

9 |

2.7 |

|

Finland |

1 |

0 |

4 |

1.8 |

1 |

0 |

2 |

1.8 |

|

Norway |

0 |

1 |

3 |

1.4 |

1 |

0 |

3 |

1.8 |

|

Ireland |

0 |

1 |

1 |

0.8 |

0 |

0 |

2 |

1.2 |

|

Austria |

0 |

0 |

3 |

0.3 |

0 |

0 |

6 |

0.8 |

|

Poland |

0 |

0 |

2 |

0.2 |

0 |

0 |

1 |

0.1 |

|

Portugal |

0 |

0 |

2 |

0.2 |

– |

– |

– |

– |

|

Hungary |

0 |

0 |

1 |

0.1 |

0 |

0 |

1 |

0.3 |

|

Greece |

0 |

0 |

1 |

0.1 |

0 |

0 |

3 |

0.3 |

|

Total |

19 |

21 |

75 |

77.8 |

23 |

18 |

100 |

90.8 |

At present, there are four clear country drivers: Germany, France, Switzerland, and Sweden. Over the past two years, these countries have noticeably increased their university potential. For example, Germany has six WCUs and four higher education establishments claiming this status and has additionally created six specialized WCUs. Thus, the German model of university science is the pattern of upward development, from specialized higher education establishments to their gradual scientific diversification, up to the creation of WCUs. Small Sweden and Switzerland have set a record of their own, three WCUs each against the backdrop of a significant reserve for further development. France has formed two WCUs against the backdrop of the increasing number of specialized higher education establishments. To all appearances, these countries will be the main catalysts of the European system of higher education.

In 2019, Norway created a WCU and thus came into the spotlight. Hopefully, Holland will restore its leading positions and will return to its previous mark of five WCUs. Obviously, Italy, Spain, and Austria have a spare capacity, two to three WCUs. In the future, Eastern European countries, for example, Poland, Hungary, and the Czech Republic, will probably also make a certain contribution. All this holds out hope that the success of Europe of the last two years will not decay into a casual deviation, growing into a stable trend.

We should recognize that the rapid strengthening of the European segment of MLU is to all appearances an extraordinary event. How can we explain it?

Answers to this question can be different, mainly hypothetical. Let us propose a possible version.

In our opinion, the success of European universities in the 21st century is determined by two factors. The first one is that the European system has a serious reserve of potential WCUs owing to its rich history of their creation and functioning. Some of such higher education establishments periodically strengthen their positions and turn into full–fledged WCUs, while others, vice versa, weaken and worsen their positions in global rankings. However, all these players of the university market can come into the spotlight anew and take the lead. In other words, Europe is strengthening not so much due to newly created higher education establishments as to the activation of old ones.

The other factor of Europe’s success is the unique combination of competition and collaboration mechanisms. We mean the wide spread of the philosophy of collaboration in the European MLU [7–9], movement toward the creation of various forms of university collaborations. Britain provides the brightest examples of such an interface of the mechanisms of power, competition, and cooperation.

For example, in 1994 it formed the Russell Group (RG), which includes the 24 most prestigious British universities and promotes interests of the member universities before the government, parliament, and other influential structures [11]. The RG is often considered as the British equivalent of the American Ivy League, which embraces the eight oldest higher education establishments of the United States. In the same year, in response to the alliance of the powerhouses of the British university sector, there emerged the 1994 Group (G–94), a coalition of 19 minor universities with intensive research [10]. Despite the initial confrontation of the two coalitions of British higher education establishments, there is no unbridgeable gulf between them: two universities from G–94 later entered into the RG.

The cooperation of British universities goes still further. In 1997, another university group appeared in the United Kingdom, the Coalition of Modern Universities, which in 2004 was renamed the Campaign for Mainstream Universities with the subsequent rebranding in 2007 into Million+, pointing to the fact that more than 1 mln students studied in the higher education establishments of the association; in 2016, the group ultimately adopted the brand MillionPlus (MP) and now includes 21 universities [14]. The coalition embraces former technology institutes, which received the status of universities after 1992 and now cooperate to defend their interests. Therefore, British higher education establishments continuously compete for a place in the market and search for channels of collaboration and forms of partnership with similar academic structures.

In addition to the above alliances, Britain is constantly creating regional university unions. For example, in 1997 the White Rose University Consortium (WRUC) was created as a partnership of three universities of Yorkshire (England) to unite their resources [12]. Collaboration implies joint studies, industrial partnerships, and scholarships for postgraduates. The WRUC created a joint electronic storage to upload dissertations and preprints of associates of the three universities, turning it into a part of the national and international Internet networks. In 2006, the WRUC and Sheffield Hallam University created Myscience. Co Ltd to manage the National Learning Center in York. All this offers the possibility to make WRUC scientific developments publicly available and thus to increase their readership, recognizability, and citation rate.

In 2007, the N8 Research Partnership (N8), a collaboration of eight research universities was created in the north of England; its members seek to develop their research frameworks by identifying and coordinating influential research groups in the region. The N8 establishes close cooperation with industry [13]. In 2013, the Science and Engineering South Consortium (SES–5) was formed, consisting of five state research universities in the southeast of England, which unite their resources and possibilities for further research in priority spheres of science and technology [16]. The SES–5 provides a network based on the 12 000–core IRIDIS Intel Westmere supercomputer cluster, available for research and scientific calculations across all its member universities.

In 2006, British outsider universities, i.e., those that had joined no other university before, formed the Alliance of Nonaligned Universities, which in 2007 adopted its current name, University Alliance (UA) [15]. Its membership is made up of 21 technical universities with a mission to drive innovation and economic growth in Britain’s cities and regions by strengthening links with business and industry. The UA maintains links with over 16000 enterprises, including 11000 small and medium-sized businesses. In 2015, the UA launched the UK’s largest multipartner doctoral training program, building on its members’ strengths in respective R&D fields. In 2018, this program was extended to include foreign students. The alliance contributes much to student enterprise. For example, according to available data, 40% of the UK’s successful graduate start–ups–those surviving beyond three years–come from Alliance graduates. In addition, in 2013 the UA concluded a partnership with the Australian Technology Network, a group of four universities; in 2017, a delegation took place to strengthen links between the two alliances.

In addition to the creation of various university unions, alliances, consortia, groups, coalitions, and partnerships inside European countries, higher education establishments of different European states form associations. For example, in 1985 the Coimbra Group (CG) was founded–an association of the oldest and most influential multiprofile universities of Europe. Its mission is to internationalize collaboration and improve the professionalism of research and education. Today the association includes 39 universities from 23 European countries with over 1.4 mln students and multibillion dollar research budget [18].

In 1992, the University of Oxford initiated the Europaeum association, which unites talented students and researchers working in the humanities and social sciences to promote academic mobility and collaboration [19]. At the beginning, the Europaeum united 12 higher education establishments from 10 European countries; today, they number 16 from 13 states, plus Central European University, Budapest, which has been included in the association on a short–term basis not as a member but to support it by establishing a special relationship. This is an example of an act of solidarity of the Europaeum with the young Hungarian university, which is facing clear difficulties.

In 2002, the League of European Research Universities (LERU) was formed as a consortium of leading science–intensive universities of Europe for knowledge and experience exchange to reach high indicators in education and research, to pursue basic research jointly, and to improve the competitiveness of European universities on the international arena [17]. At first, LERU included 12 European universities; in 2010, their number increased to 21 and, then, to 23.

The above examples do not cover integrative initiatives of European higher education establishments; they merely illustrate the process of “growing” WCUs through the large–scale diffusion of scientific results and advanced methods of the organization of research. It is safe to assume that this policy has made it possible to turn the European university space into a boiler continuously heated by new initiatives and interactions.

The weakening core of the Small British Union. The territorial cluster of the SBU is in a state of clear turbulence. This is manifested in differently directed trends of the development of the union’s national university systems (Table 4). For example, observable is a slight weakening of the positions of Australia and New Zealand, accompanied by the clear deterioration of the indicators of the United States against the background of the strengthening of Canada and Britain. Note that the development of Canada, Australia, and New Zealand has practically reached its peak: in the near future, a new WCU can appear only in Canada, while a more significant effect is possible only in the long term. However, the existing results allow us to speak, for example, about the Australian miracle, when a country relatively small in terms of population and distant from the civilizational meridians has become a champion regarding the number of WCUs, yielding only to the United States and Britain and outrunning Germany and China.

Table 4. Comparison of the SBU university systems

|

Country |

2017 |

2019 |

||||||

|

U–1 |

U–2 |

U–3 |

W |

U–1 |

U–2 |

U–3 |

W |

|

|

United States |

38 |

16 |

36 |

371.2 |

36 |

14 |

47 |

346.7 |

|

Britain |

17 |

1 |

39 |

126.5 |

18 |

0 |

41 |

138.4 |

|

Canada |

4 |

2 |

8 |

31.8 |

5 |

1 |

9 |

32.4 |

|

Australia |

7 |

0 |

17 |

29.6 |

7 |

0 |

14 |

29.1 |

|

New Zealand |

1 |

0 |

6 |

3.4 |

1 |

0 |

4 |

2.6 |

|

Total |

67 |

19 |

106 |

562.7 |

67 |

15 |

115 |

549.3 |

To all appearances, the Australian and, partially, Canadian miracles rest on the same mechanism as in Europe. Suffice it to say that in 1999 the Group of Eight (Go8) was formed, a coalition of the largest and oldest universities of Australia [20]. According to the existing data, in 2008 the Go8 received almost twice as much research funding as the other 31 Australian universities combined. Seventy–three percent of the Australian Competitive Grant subsidies went to the Go8; it is this group that yields the most research results assessed at categories 4 and 5, i.e., higher and much higher than the world standard; and 99% of the group’s studies fall into the category of the world class and higher. The Go8 annually spends about $6 bln for research, $2 bln of which goes to developments in medicine and health care. It is assumed that the Go8 ensures a multiplier of the national economy by almost ten units; i.e., every dollar of research income gives $10 of the GDP. In addition, the Go8 is a member of numerous international alliances and a party in numerous agreements with universities and research organizations across the world. In addition to the Go8 alliance, other university associations work in Australia: the Regional Universities Network of six universities, founded in 2011 [21]; the network Innovative Research Universities of seven universities, established in 2003 [22]; and the Australian Technology Network made up of four technological universities from each continental state of the country, which was formed in 1975 and restored in its present form in 1998.

In Canada, network collaboration between universities is less expressed, but Canada, too, has unions of its own, for example, the Group of Canadian Research Universities of the country’s 15 leading universities, formed in 1991. All this gives grounds to believe that the SBU universities will preserve their leading positions in the long term.

Against this backdrop, the United States is of special interest. The point is that the trend of the last two years testifies to the beginning decline of the US MLU. This is shown by the shrinkage of two of its segments (U–1 and U–2) against the backdrop of the expansion of the third segment, U–3. This means that the traditional trend toward the assemblage of multidisciplinary WCUs from specialized institutes has reversed, launching the disintegration of global scientific centers into numerous specialized organizations. If the United States does not renew the trend toward the concentration of its scientific potential, the number of the country’s WCUs will gradually decrease, thus decreasing the significance of America in global science.

For fairness sake, let us note that the philosophy of collaboration remains the exclusive province of Europe and SBU countries. Although moves toward interuniversity collaboration is observable everywhere, including Asia, they are rudimental there. For example, in 1998, China created the C9League (C9), an alliance of nine universities in mainland China. However, as opposed to European and SBU countries, the C9 was initiated by the country’s central government. In aggregate, the C9 universities embrace 3% of all researchers, receive 10% of national expenditure for science, and generate 20% of the country’s scientific publications and 30% of all citations. An official newspaper of the Communist Party of China, The People’s Daily, calls the C9 “China’s Ivy League” [24]. Note that there are four categories of elite universities in China. The first includes 116 leading higher education establishments; the second one, 42 “Double First–Class” universities; the third, 39 most competitive establishments; and the fourth, the C9 group. Thus, competition and integration processes in China are well under way, but they rest not on the universities’ self–government and initiatives but use directive mechanisms of the central government.

Outsiders of the university market: Running on empty and drifting backward. There are regions on the map of the world that are either fully or nearly absent in the WCU market. These are Africa and the Middle East in the first place, which have no WCUs. In 2019, only one state in Africa, South Africa, has three specialized world–class institutes. In the Middle East, the situation is hardly better: Saudi Arabia and the United Arab Emirates have one specialized international-level higher education establishment each, and Israel, one university claiming WCU status. However, even these modest figures have a second bottom: the situation in 2019 became worse compared to 2017 (see Table 1). Thus, the above two geographical regions are unable thus far to catch up with modern civilization even at the local level.

Another two geopolitical regions–Latin America and the former Soviet republics–are almost absent in the WCU market. They have one WCU each (Brazil and Russia, respectively). Note that the situation in Latin America is much better than in the post–Soviet space. Argentina has a higher education establishment claiming WCU status, and another three countries are represented in the market by six specialized world– level institutes (Table 5). The post–Soviet space lacks any geopolitical diversification, and the entire contribution is ensured by one country, Russia. Note that comparison between Table 1 and Table 5 shows a striking similarity in the dynamics of the university systems of Russia and Brazil: all their indicators were equal and tended to decrease.

Table 5. Comparison of the university systems of Latin American countries

|

Country |

2017 |

2019 |

||||||

|

U–1 |

U–2 |

U–3 |

W |

U–1 |

U–2 |

U–3 |

W |

|

|

Argentina |

0 |

1 |

1 |

1.1 |

0 |

1 |

1 |

1.1 |

|

Brazil |

1 |

0 |

4 |

2.4 |

1 |

0 |

2 |

2.1 |

|

Colombia |

– |

– |

– |

– |

0 |

0 |

2 |

0.2 |

|

Mexico |

0 |

0 |

2 |

1.4 |

0 |

0 |

1 |

1.3 |

|

Chile |

0 |

0 |

3 |

1.2 |

0 |

0 |

3 |

0.7 |

|

Total |

1 |

1 |

10 |

6.1 |

1 |

1 |

9 |

5.3 |

However, the comparison of Russia with Brazil is in favor of the latter. This is due to the higher status of the University of Sao Paulo compared to Moscow State University. The former occupied 79th place in the WCU ranking after having lost five positions, while the latter, 107th place, eight positions having been lost. In addition, the University of Sao Paulo was in the QS subject rankings in nine disciplines, while Moscow State University, only in five, which is the trimming line. This means that if Moscow State University loses another subject, which did occur in the past two years, it will lose WCU status. In this case, not only will Russia disappear from the WCU market but so will the entire post-Soviet space. Considering recent trends, this risk is rather high, while for Brazil and Latin America as a whole, such an outcome is improbable.

Global high–tech companies and WCUs: Parallels in development. The literature earlier noted an interesting parallel between the number and strength of two types of organizations–WCUs and global high–tech companies (GHTCs) [25]. To be more definite, by GHTCs we will hereinafter mean major, very famous, and globally recognized companies of respective countries, which relate to the producing sector (banking, insurance, consulting, retail, etc., are excluded) and are characterized by high technology indicators (extracting and construction companies are not considered). The introduced clarifications make it possible to concretize the general hypothesis: the number of a country’s WCUs approximately coincides with the number of its GHTCs. The number of WCUs for different countries is given in the Ranking of World–Class Universities [1], while the determination of the number of GHTCs is an independent analytical problem, which can be solved only conditionally at the qualitative level. Note that our hypothesis does not imply either a direct relation between WCUs and GHTCs or their mutual support; they rather interact indirectly, which does not cancel parallels in their establishment and development.

The formulated hypothesis shows a country’s true drivers for the emergence and stable functioning of WCUs. In this context, let us turn to some styled examples that demonstrate the outlined parallels.

Thus, South Korea has three WCUs: Seoul National University, Korea Advanced Institute of Science and Technology, and Sungkyunkwan University, each of which is stronger than Moscow State University. Note that there are three global South Korean companies known across the world: Samsung Electronics, Hyundai Motor, and LG Electronics, which in 2010 enjoyed the highest capitalization and sales among all companies of the country and were the main employers for the local population. If we consider that Samsung Electronics and LG Electronics appeared in the 1930s and Hyundai Motor, in the second half of the 1940s, it will become clear that South Korea had enough time to create three powerful universities to provide personnel for the three industrial giants, two of which represent the electronic industry and the third one, machine building. Thus, we see a clear correlation between WCUs and GHTCs. Meanwhile, ties between the two types of organizations are not that trivial. For example, in 2017, South Korean WCUs included Korea University, replaced in 2019 by Sungkyunkwan University. This means that the WCU market, as well as the GHTC market, is very mobile: higher education establishments compete for ties with industry, and global leader companies are ousted from their positions by immediate competitors. All this leads to castlings and interchanges in both markets. For example, the appearance of new powerful GHTCs is bound to lead with time to the growth of WCUs, and, vice versa, the degradation of the sector of innovation-oriented corporations leads to the destruction of the MLU.

A similar situation is observed in Singapore, where, along with two powerful WCUs (National University of Singapore and Nanyang Technological University), there are two major transnational corporations–Singapore Telecommunications and Wilmar. The former was founded in 1879 and is the country’s largest mobile operator and Internet provider with representations in other countries, the number of clients totaling 0.5 bln people. Wilmar is assumed to be the largest agroindustrial company in Asia, producing palm oil and other vegetable oils based on the wide use of biotechnologies. The scale of the company’s activity is such that in 2012 Newsweek recognized it the worst in the world because of its negative impact on the environment owing to deforestation, peat mold drainage, and the exploitation of the local population in plantations of Indonesia. Thus, the rapid development of Singapore’s two WCUs proceeded in parallel with the development of the above two industrial giants.

An interesting example is one WCU of Finland (the University of Helsinki), the economic potential of which is rather small. This phenomenon can be explained by the legendary company Nokia, which became the leader in the global mobile network market and the country’s preeminent brand and for a long time had sales with which other Finnish firms were unable to compete. Considering that Nokia appeared in 1865, Finland also had enough time to adapt its university system to the requirements of the high–tech giant.

A similar situation exists in Brazil with its only WCU, the University of Sao Paulo. At the same time, Brazil is famous for its aerospace company Embraer S.A. (Empresa Brasileira de Aerondutica S.A.), which produces military, executive, and agricultural aircraft and has become a leader in the global market of passenger regional airbuses. Today Embraer competes with the Canadian company Bombardier for the right to be the third largest producer of civil aircraft after Airbus and Boeing. The time span from the foundation of the company, 1969, to the present day was just enough to form demand for high–tech personnel prepared in the university sector. Noteworthy is the fact that Embraer is headquartered in Sao Paulo, where the Brazilian WCU is located.

A bright example of the interface between the two markets is Switzerland, where three strong WCUs–ETH Zurich (Swiss Federal Institute of Technology), Swiss Federal Institute of Technology Lausanne (EPFL), and the University of Zurich–form the background for three corporations with three–digit indicators of market value (hundreds of billions of dollars): the food company Nestld, the pharmaceutical company Novartis, and the pharmaceutical and diagnostic corporation Hoffmann–La Roche. The achievements of Novartis in the high–tech sphere made front–page headlines worldwide: in 1982, Sandimmune, an immunosuppressant medication, was created, which led to a sharp increase in the number of organ transplantations across the world; Gleevec became a breakthrough in the treatment of chronic myelogenous leukemia; and Coartem, designed to treat malaria, became the first Artemisinin–based strong combination drug available for state purchases. The wide product and technological diversification of Nestld was accompanied by mergers with other high–tech firms. For example, in 2006, Nestld purchased the subdivision Medical Nutrition from Novartis for $2.5 bln, which ultimately secured its status as a high-tech company. Hoffmann–La Roche is a leading producer of biotechnological drugs in oncology, virology, rheumatology, and organ transplantation and has representations in 150 countries with a staff of 95000 employees.

Germany also falls into the regularity under consideration: it has an impressive potential of six WCUs (Ludwig Maximilians University of Munich, Heidelberg University, Technical University of Munich, Humboldt University of Berlin, Free University of Berlin, and RWTH Aachen University) and a respective pool of six high–tech corporations. If we select high-tech firms from among Germany’s largest and most famous companies, the following six firms will undoubtedly have GHTC status: Volkswagen, Siemens Group, Daimler, BMW Group, Deutsche Telekom, and Bayer. Other German high-tech giants are behind the above six, although they also claim a leading role and thus lay grounds for the appearance of new WCUs. Note that the technological leadership of Germany manifests itself especially clearly in its successes in the market of technical higher education, which again confirms the hypothesis under test.

The list of such examples could go on, but the main point is that even a superficial test of the hypothesis about a correlation between WCUs and GHTCs yields data that support it. This means that it is real production that is the customer of various innovations and highly skilled personnel, the latter being prepared by WCUs for the needs of GHTCs and sometimes with their direct participation. This allows us to formulate the following formula: where there are GHTCs, there are WCUs.

The rise of Europe: A tendency or a deviation? The above–considered shift of the global system into universities of Europe is a phenomenon of great geopolitical significance. In fact, the picture is as follows: Arrighi’s first three cycles of capital accumulation proceeded on the territory of Europe, the fourth one was formed and is coming to an end in North America, and the future fifth cycle will return to Europe. Thus, the civilizational spiral of capital movement closes in a very narrow geographical zone. Note that, as opposed to the previous four cycles, when the center of capital was in a concrete country, the new center is crystallizing due to the consolidation of different countries on a territory with a single cultural foundation.

At the same time, the outlined trend raises numerous questions and doubts. For example, we analyzed only two points–2017 and 2019. Are conclusions based on such a short period reliable? Is the success of the EU not a temporary phenomenon or an accidental deviation in the distribution of the intellectual capital of the world system?

To clarify, at least somehow, this point, it is useful to turn our attention to the global royalty trade. To this end, let us compare the exports and imports of intellectual property (IP) rights of two global players (the EU and the United States) in recent years (Table 6, based on data from [27]). We see that the last five years saw a castling of the US and EU positions. In 2012, the United States was vastly superior to Europe in IP sales, while in 2017 the situation was different. This confirms that the European Union is consolidating the creation of technological innovations. Although figures say nothing about the quality of developments in different regions and the relation of their pioneering properties, the very fact of the intensification of this activity in European countries is beyond doubt. The activization of the royalty and university system markets in the EU may be two sides of the same coin. In this case, the trend toward the strengthening of the European university market can persist.

Table 6. Comparison of the income/expenditure of the United States and the European Union from IP right trade, bln dollars

|

Years |

IP right exports |

IP right imports |

IP right balance |

|||

|

United States |

European Union |

United States |

European Union |

United States |

European Union |

|

|

2012 |

124.4 |

98.2 |

38.7 |

129.3 |

85.8 |

–31.1 |

|

2017 |

128.4 |

129.3 |

51.3 |

191.4 |

77.1 |

–62.1 |

* * *

Thus, the second stage of WCU identification has made it possible to establish that the world is actively reformatting the market of leading universities. An unexpected fact is that Europe has turned into the regional leader of the global market. Equally unexpected is the slowdown in the development of the Asian WCU segment. The value of Russia in the MLU remains vanishingly small; in 2019, its contribution by the integrated estimate was 0.2% of the global market.

The above case analysis makes it possible to identify two important drivers of a national WCU system: external, which means that this country has GHTCs that form demand for skilled personnel and innovative developments; and internal, i.e., the wide use of the philosophy of collaboration by universities themselves, which allows them to adopt and process creatively the best practices of their direct competitors. In a wide sense, the philosophy of collaboration generates an amazing mixture of competition and mutual assistance, which turns the zero–sum game into a positive–sum game. This social practice leads, according to B.R. Clark, to the generation of ambitious collective will [26], which sustains a series of successful initiatives inside universities and creates an all-encompassing aura of success. Using a rough analogy, we can say that the presence of the external driver acts as a necessary condition for the creation of a WCU, while the presence of the internal one serves as a sufficient condition. Any attempts to evade these two factors of university system development are fraught with idle efforts because it is impossible to create national WCUs with no economic and cultural foundation.

References

1. http://nonerg-econ.ru/cat/16/201/. Cited April 29, 2019.

2. http://nonerg-econ.ru/cat/16/203/. Cited April 29, 2019.

3. E.V. Balatsky and N. A. Ekimova, “Identification of world class universities,” Mir Novoi Ekon. 11 (3), 81— 89 (2017).

4. E. V. Balatsky and N.A. Ekimova, “World class universities: Experience of identification,” Mir. Ekon. Mezhdunar. Otn. 62 (1), 104–113 (2018).

5. G. Arrighi, The Long Twentieth Century: Money, Power, and the Origins of Our Times (Verso, London, 1994).

6. G. Arrighi, Adam Smith in Beijing: Lineages of the Twenty–First Century (2007).

7. V. M. Polterovich, “Positive collaboration: Factors and mechanisms of evolution,” Vopr. Ekon., No. 11, 1–19 (2016).

8. V. M. Polterovich, “Towards a general theory of socioeconomic development. Part 1. Geography, institutions, or culture?,” Vopr. Ekon., No. 11, 5–26 (2018).

9. V. M. Polterovich, “Towards a general theory of socioeconomic development. Part 2. Evolution of coordination mechanisms,” Vopr. Ekon. No. 12, 77–102 (2018).

10. http://www.1994group.ac.uk/. Cited April 29, 2019.

11. https://www.russellgroup.ac.uk/. Cited April 29, 2019.

12. White Rose University Consortium. https://whiter- ose.ac.uk/about/. Cited April 29, 2019.

13. https://beta.companieshouse.gov.uk/compa-ny/05920709. Cited April 29, 2019.

14. https://university.which.co.uk/advice/choosing-a-course/what-is-the-million-group.Cited April 29, 2019.

15. University Alliance. https://www.unialliance.ac.uk/.Cited April 29, 2019.

16. Science and Engineering South Consortium (SES–5). https://www.ucl.ac.uk/news/2013/may/science-and-engineering-south-consortium-ses-5. Cited April 29, 2019.

17. League of European Research Universities. https://www.leru.org/. Cited April 29, 2019.

18. The Coimbra Group: A tradition of innovation. https://www.coimbra-group.eu/. Cited April 29, 2019.

19. Europaeum. https://europaeum.org/. Cited April 29, 2019.

20. Group of Eight. https://go8.edu.au/. Cited April 29, 2019.

21. Regional Universities Network. http://www.run.edu.au/. Cited April 29, 2019.

22. Innovative research universities. https://www.iru.edu.au/. Cited April 29, 2019.

23. Australian Technology Network. http://www.atn.edu.au/. Cited April 29, 2019.

24. China’s Ivy League: C9 League. http://en.peo- ple.cn/203691/7822275.html. Cited April 29, 2019.

25. E. V. Balatsky, “World–class universities and global high–tech companies: Parallels and correlations,” in Interdisciplinarity in Modern Sociohumanitarian Knowledge 2017 (Izd. Yuzh. Fed. Univ., Rostov–on–Don, 2017), pp. 208–226 [in Russian].

26. B. R. Clark, Sustaining Change in Universities: Continuities in Case Studies and Concepts (Open Univ. Press, Maidenhead, 2004).

27. World Development Indicators. https://datacata-log.worldbank.org/dataset/world-development-indi-cators. Cited April 29, 2019.

Translated by B. Alekseev

Official link to the article:

Balatsky E.V., Ekimova N.A. Geopolitical Meridians of World-Class Universities// «Herald of the Russian Academy of Sciences», 2019, Vol. 89, No. 5, pp. 468–477.